Daily Roundup: Paytm and Cockroach portfolio

Business, Finance

Why the lukewarm response to Paytm IPO?

Business

It has been a bustling last couple of weeks at Dalal street, with IPOs pouring in left, right, and center. While many startups such as Nykaa, Policybazaar, Latent View Analytics, and Paytm made their much-anticipated IPO debut, several other companies such as Droom and Delhivery are busy filing their pre-IPO papers.

Of all the companies, the homegrown financial services company - Paytm, is raking in the most amount of attention - but for all the wrong reasons. Touted to be the biggest of the country so far, Paytm IPO failed to live up to its hype and expectations.

The lackluster listing day

The market debut of Paytm is disappointing, to say the least, with the stock now trading at a discount.

The opening price of the stock on BSE is INR 1950 which is 9.3% less than its issue price of INR 2150. The stock further dipped by 26% to reach an intraday low of INR 1586.

Macquire, a foreign brokerage firm, predicts that the stock is likely to witness a further fall settling at a share price of INR 1200 - a 44% low from its issue price!

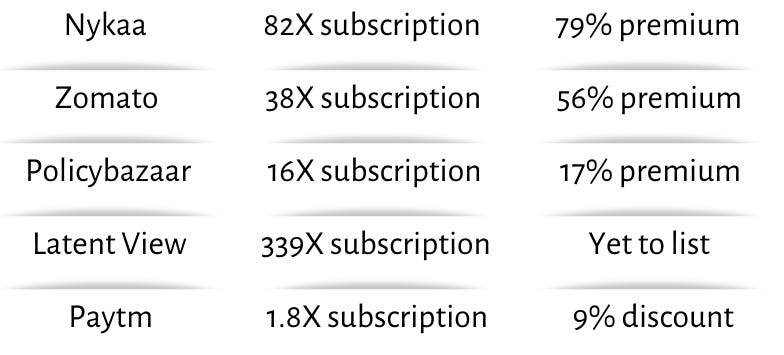

The listing numbers were anticipated by market analysts after the stock received a tepid response in its IPO subscription having been subscribed only 1.8X times.

Paytm v/s other Indian startups

The subpar response comes as a crude shock to the company’s investors because the market sentiment towards startups has been largely positive in recent times.

While Nykaa and Zomato had blockbuster listings, making their founders billionaires overnight, the same did not apply to Paytm and its founder Vijay Shekhar Sharma.

Despite being around for two decades, having a significant brand recall, and building a ubiquitous network of financial services, why is Paytm given a bland welcome by investors?

While a lot is being speculated as to the reasons for the dull performance, we attribute three primary reasons that might have significantly affected the stock performance.

Missing out on the UPI gold mine

Demonetization was a watershed moment for Paytm. Stripped of physical cash, citizens flocked to the Paytm application for their day-to-day transactions. However, Paytm’s moment in the sun did not last very long.

A superior, customer-friendly and government-promoted UPI technology pulled all the demand for digital payments - severely wounding the primary business model of Paytm, walled-based digital transactions.

In the UPI race, Paytm is a distant number three player, with PhonePe and Google Pay ruling the roost.

Jack of all, master of none!

With its wallet business faltering, the company diversified its business across the finance ecosystem: e-commerce (Paytm Mall), payment bank, insurance, stockbroking, digital gold, movie tickets, mutual funds and much more!

Though diversification sounds good on paper, Paytm failed to become profitable or the market leader in any of its multiple categories.

The investors could never understand what exactly was Paytm’s business model and what was the company’s golden egg. The company struggled to pave out a clear path to profitability.

Timing and pricing the IPO

Paytm waited a tad bit long to go public.

With several companies queueing up to go public, retail and institutional investors have many choices to place their bets on. The likes of Nykaa and Latent View Analytics which already recorded profits are preferred over Paytm which never recorded a single penny of profit.

With no sight of near-term profitability, market analysts also feel that Paytm stock is overpriced.

What's next?

The Indian market is witnessing a never-seen-before bull run.

For a while, it seemed like investors would lap in anything and everything that is moving on the bourses irrespective of the company’s finances. But the story of Paytm IPO proves that logic and rationale still prevail in the markets!

For the companies waiting in line to go public, the Paytm narrative would serve as a cautionary tale.

The cockroach portfolio: A portfolio for all seasons

Finance

What if we told you that there is an investment portfolio designed for all types of economic scenarios?

Any period of recorded economic history, in any country in the world, can be categorized into one or a combination of these four environments as shown -

The most common portfolio construction is a stock and bond focused approach (60% stocks and 40% bonds).

But, stocks- and bond-focused portfolios only thrive in two of the four mentioned quadrants – stocks do well in periods of growth and bonds do well in periods of deflation (reverse inflation).

'The Cockroach Portfolio' is a portfolio designed to survive in all types of economic scenarios.

Coined by one of the most influential financial writers, Dylan Grice, it is derived from the nature of cockroaches – they are physically hardy and use a simple way to survive.

The cockroach portfolio uses four assets to survive the vast majority of economic outcomes — stocks, bonds, gold, cash.

The cockroach portfolio will simply allocate money equally across these four assets (25% each).

The cockroach portfolio seeks to survive (but not necessarily thrive in) all types of economic scenarios:

Normal times, when the economy is expanding, it uses stocks to survive

Recessions or depressions, when the economic outlook is negative, it uses cash to survive

It uses bonds to survive deflation

Finally, it uses gold to survive inflation

It's as simple as that!

Let’s take a look at how this portfolio has performed over the past few years (the purple line in the graph). The cockroach portfolio did okay compared to other portfolios. But that’s the point of the cockroach portfolio – to survive.

Let’s take a closer look at how the cockroach portfolio fared during the 2020 COVID market crash (red line in the graph). For lower risk compared to 60-40 stock/bonds, the cockroach survived the COVID market crash in the face of Treasury Bonds. The cockroach survives economic downturns.

Like what you read? Share this article with your friends and follow us on:

Instagram | Medium | LinkedIn